To say the payments industry is going through disruption is certainly not a hyperbole these days. The fundamental shifts in how commerce gets done have begun to impact the way payments have been done all these years. On the one side, the payments industry has seen the entry of diverse fintech players, including giants like Facebook and Tencent, in addition to the start-ups that are presenting increased competition for banks and corporations. On the other, the threat from fintechs is being further fuelled by rapidly evolving customer expectations, which continue to push the boundaries for the industry as a whole. It is increasingly apparent that the payments marketplace will look fundamentally different a decade from now. There will be new form factors, real-time infrastructure, greater levels of integration with social media and e-commerce, to name a few of the changes. In effect, the revolution that has completely disrupted the consumer payments industry over the last decade or so is finally coming to take into its fold the corporate payments industry, too.

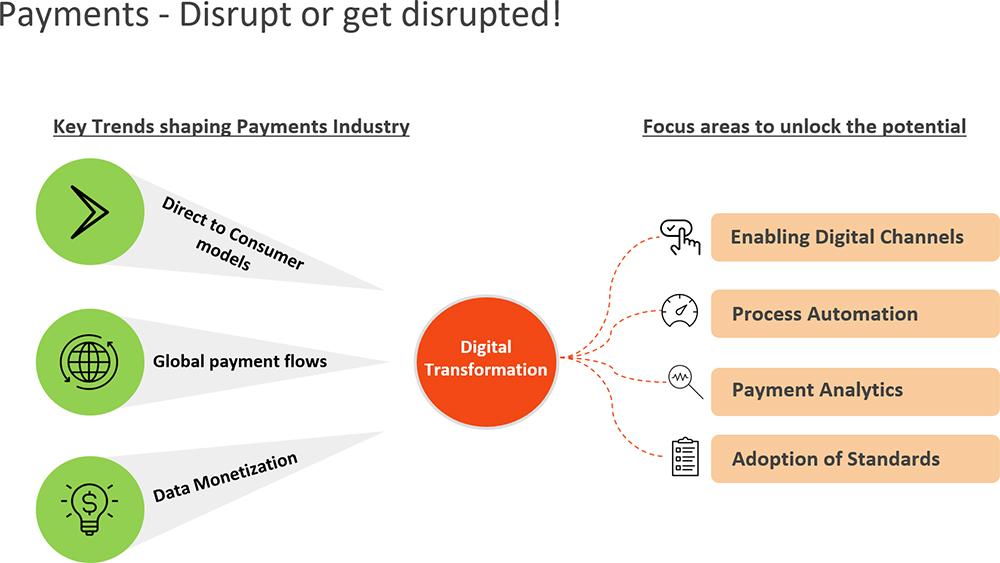

I see three big trends that are likely to shake up this segment, which is at half a trillion dollars a year, and growing:

- Direct-to-consumer models: As firms across industries move to direct engagement with their customers, it is becoming increasingly necessary to deliver them the same level of digital experiences as the consumer payments industry does.

- Global payment flows: Cross-border payments now make up over 10 per cent of all corporate payments, and they are growing. These flows are almost always digital in nature, with the added complexity of regulatory compliance and risk management.

- Data monetization: Bank treasury services have had the advantage of managing and servicing fund flows between their corporate clients. And as these fund flows become increasingly digital, they have enabled banks to build a data goldmine. Banks are now actively looking to leverage this data to deepen their service offerings.

Banks and corporations have started responding to the call of digital, and the payments processing industry is currently going through a wave of infrastructure modernization. I see significant technology investments by CIOs across firms that are setting the stage for the next wave of digital transformation. The payments industry will look fundamentally different a few years from now. By adopting digital channels, embracing automation, adopting open standards and making smart bets in technology, banks and corporations can emerge as winners in the payments marketplace.

Making digital transformation happen

As digital transformation initiatives in payments pick up steam, there are four main areas of focus, each of which is important to ensure not just a solid foundation for a digital payments ecosystem, but also to ensure the groundwork for unlocking the revenue potential from treasury and payment operations. This is something yet to be tapped in most organizations:

- Enabling of digital channels: Buoyed by the consumer payments industry, there is a rapidly growing array of digital payment channels that need to be integrated into the digital payments service offerings.

- Process automation: Payment processes typically span across entities (bank-corporation-consumer), and integration across disparate systems will make for a critical foundation to enable scalable implementations.

- Payment analytics: Payment processes have always been data rich, and even more so when digital channels continue to grow. Effective use of the data to make better decisions (e.g., manage risk, prevent fraud) and, furthermore, explore data monetization opportunities, are becoming important.

- Adoption of standards: For any multi-entity ecosystem with entities across the globe to scale with technology, it is essential to establish standards. Adoption of open banking standards is essential for digital payments to succeed – and we are at an inflection point, given the increasing adoption of these standards.

Digital channels

The ubiquitous cheque has been the staple in corporate payments for years now. Despite being the most expensive payment instrument, the cheque has dominated the corporate payment world for decades. It is not just the processing cost of the paper cheque that makes it a burden for banks. It is also a security headache. It is well known that paper cheques are the largest vehicle of payment fraud.

All that is changing. And, as it usually happens, this started with the consumer payments business. As the direct-to-consumer models continue to evolve, the B2C payments business is growing rapidly (annual growth rate of 15 per cent led by digital e-commerce)6. And the digital payment technologies that are coming out of the consumer payments industry (Zelle, Paypal, digital wallets, et al) offer a rich choice for banks and corporates to offer digital experiences to their customers:

- Disbursement of funds: Transfer volumes of Medicare/Medicaid funds by healthcare providers to their members continue to rise and should, by and large, be digital.

- Refund management: In a direct-to-consumer world, corporations need to manage refunds to customers from excess payments and product returns. Customers used to instant digital payments from the e-commerce world are expecting a similar experience everywhere.

- Loyalty/reward disbursements: As corporations build deep relationships with their customers, they continue to adopt customer engagement strategies from e-commerce retailers. These include cash-back payments and encashing of loyalty points, which need to be executed through digital channels. A similar revolution is around the corner in B2B payments, with the expansion of consumer-like payment rails, such as digital wallets, in addition to the existing ones like ACH, Wire, virtual cards, etc. We believe the convenience of digital payments is only a starting point. There is so much more to it by way of benefits:

- Streamlining of payment processes has a direct impact on working capital management. Trade finance is key to enabling global supply chains, and fintechs are coming up with specific solutions.

- Cross-border payments to suppliers and subsidiaries need to stand up to heavy regulatory requirements in addition to managing the risk of fraud. Digital payments are increasingly the safest alternative. In addition to enforcing compliance, digital channels can ensure transparency of global fund flows

- Of late, acquiring a deeper understanding of the supplier ecosystem has become an important factor (see the section on payment analytics below).

Automation

70 per cent of corporate treasury and payments professionals list manual and inefficient processes among their top challenges. In addition to their high costs, manual processes are also error-prone, difficult to scale in response to variable volumes, and increasingly susceptible to fraud.

Process simplification and automation opportunities extend across the value chain – from establishing the payment exchange with suppliers (B2B) and consumers (B2C) to creating a variety of services around three-way (PO, invoice and receipt) matching, and all the way to the disbursement of funds through different digital payment channels. Several fintechs see this as a big area of opportunity and are building to this end auxiliary platforms that can integrate with corporate systems and automate the end-to-end processes.

Bank treasury services offer a slew of products and services – from cheque processing to ACH/Wire – to their corporate clients. For instance, a large bank helps one of the largest healthcare providers in the US process over 4 million transactions on an annual basis, covering their entire value chain, from providers – corporate hospitals (B2B) and individual doctors (B2C) – to pharmaceuticals (B2B).

- There is a clear opportunity to digitally onboard these entities onto the payments network in a rapid, secure manner using DIY portals as well as create an ‘omni-channel’ like experience that minimizes onboarding friction.

- Automating a payment network of this size and complexity is undoubtedly an integration challenge, given the multiple legacy systems at enterprises and, increasingly, ERP systems. With the increasing adoption of API (application programming interface)-based data exchanges, end-to-end automation with multiple payment rails is a necessary building block for digital payments.

Data and analytics

Payment processing through digital channels is data rich: strategies and execution led by analytics on the transaction data can help in a variety of ways: improving revenues, cutting operating costs, detect fraud and other anomalous behaviour.

Risk and fraud analytics: As payments migrate to digital platforms, it is almost inevitable that fraud becomes more sophisticated too. And, as the volume and complexity of payments grow, fraud is becoming just as hard to track, identify and prevent. Fraud prevention will have to move beyond transaction-centric assessment to leveraging AI for detection and prevention of emerging fraud. Broadly speaking, organizations need to think of payments fraud at two levels:

- Account fraud: Digital identity theft is a leading cause of fraud. Methods like ATO (account takeover) and synthetic identity creation can be used to gain access into accounts and siphon funds. Tracking and preventing this requires going beyond the traditional knowledge-based authentication methods to monitor authentication journeys, looking for anomalous patterns.

- Phantom payments: Businesses lose significant amounts to fraudulent payments, triggered both by employees (e.g., initiating a phantom payment) or payees (e.g., creating double invoices). Monitoring and flagging them requires a range of methods, starting from rule-based systems (e.g. proximity of transaction requests) to more sophisticated machine learning methods (e.g., payee behaviour risk-scoring and setting of guard-rails sensitive to each risk segment).

Data monetization: A bank managing the payment flows between its corporate clients and their network of suppliers and customers has the unique ability to understand the financial behaviour of all the firms in this network. This can be a powerful tool for the bank to develop targeted strategies to drive superior experience and value for its clients:

- Working capital optimization: Banks can help their clients optimize their working capital by forecasting fund flows and using that to transfer the optimal funds into their payment accounts.

- Service bundling: Using a combination of behavioural and transactional patterns, banks can help define optimal service bundles for their clients. For example, corporate payments that span multiple countries can be optimized with a combination of exchange-rate hedging and currency-float solutions.

Adoption of standards

Open Banking

Starting in 2015, when the European Parliament adopted open banking standards (PSD2), there has been a growing momentum in adoption of standards. And, as it happens with standards, this can catalyse innovation and efficiency across the world of payments once they reach a critical mass of adoption. Open banking regulations require banks to open up their systems and data to third-party providers through secure channels. This has the potential to accelerate:

- Seamless transfer of funds between banks, using standards as opposed to relying on the current custom of point-to-point software integrations.

- The capability of corporations with multiple bank accounts across currencies to efficiently aggregate bank account data into a single accounting portal for automated reconciliation, mitigating issues in one of the most complex of payment transactions – crossborder payments.

Blockchain technology

Several financial services firms are increasingly looking to blockchain technology to mitigate the risk of fraud. The three fundamental underpinnings of the technology are distributed ledger, and immutable and permissioned access. Taken together to underpin a payment processing service, they make it possible to trace the entire sequence of wire transfers. Visa launched its B2B Connect Platform based on a private blockchain with the aim of enabling faster cross-border payments. Similarly, a host of banks, including HSBC, BNP Paribas and ING, launched Contour, a blockchaininspired platform designed to make the $18-trillion trade finance market more efficient and secure. I expect this space to see a lot more action in the coming years.

After decades of plodding along with archaic systems, the $2 trillion behemoth that is the global payments industry, is waking up, shaken up by the fintechs (a revolution of sorts that PayPal ignited).12 And, as it often happens, innovation in one sector rapidly spills over to adjacent areas; the dramatic change that started in consumer payments created the technology building blocks for digital disruption in corporate payments too. Combined with the adoption of standards and, most notably, the maturity of blockchain technologies, the corporate payments industry is primed for a burst of innovation.